AI for accounting teams is real. The problem is that the market makes it hard to tell where it is genuinely useful and where the claims are running ahead of reality.

Every accounting software company now talks about AI. Every finance platform has added AI language to its product pages. Most demos look polished. Most promises sound efficient, modern, and inevitable. But once those tools get dropped into real accounting environments, with messy source data, inconsistent processes, legacy systems, and actual review requirements, the differences show up quickly.

Some use cases are already producing measurable value. Others still look better in a sales conversation than they do in production. That distinction matters more than most teams realize. If you know where AI is already working, you can invest with confidence and get practical gains. If you do not, it is easy to end up with software that sounds impressive but never becomes part of the real workflow.

I have seen both sides of that. I have implemented AI in finance environments, and I have seen where it holds up once the novelty wears off. The most useful way to think about AI in accounting is not as a broad category, but as a set of specific workflows. Some of those workflows are structured enough, repetitive enough, and reviewable enough for AI to perform well. Others still depend too heavily on judgment, edge cases, or fragile inputs to trust yet.

Where AI is already working for accounting teams

The strongest use cases in accounting tend to share a few characteristics. The underlying inputs are structured. The outputs are verifiable. And the consequences of a miss are visible enough that a human reviewer can catch them before the mistake spreads through the system.

That is why some categories are moving faster than others.

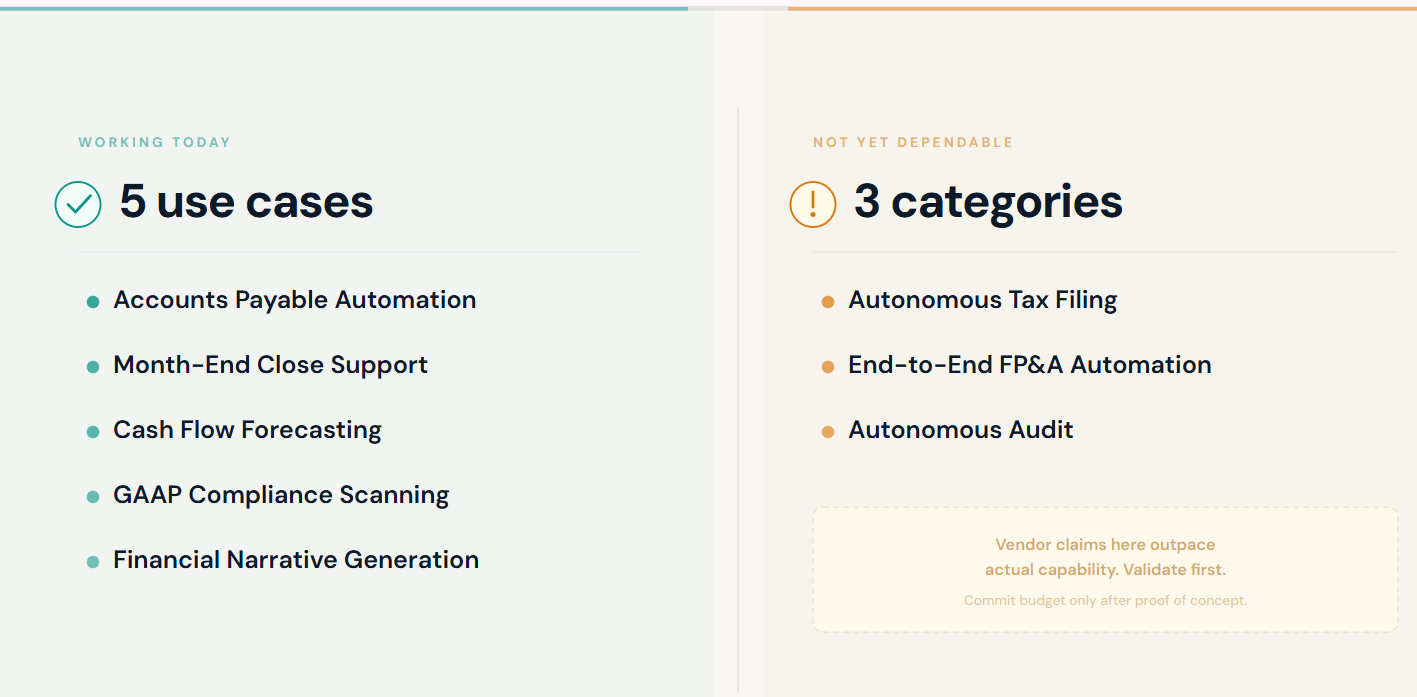

Accounts Payable Automation

If you want the clearest example of AI working in accounting right now, start with accounts payable.

This is one of the most mature and consistently valuable use cases in the finance function. AI can assist with invoice ingestion, vendor matching, coding suggestions, exception flagging, approval routing, duplicate detection, and payment workflow support. Those tasks are repetitive, they follow recognizable patterns, and they already sit inside a review process. That makes them a much better fit for automation than categories that depend more heavily on interpretation.

The time savings can be significant. In L.E.K. Consulting’s 2025 Office of the CFO Survey, one finance leader described a task that used to take three hours now taking 15 minutes with AI support. That is the kind of improvement that gets attention because it is concrete and operational, not theoretical. The same survey points to invoice processing and AP automation as one of the clearest current examples of finance AI creating real value. (lek.com)

There is adoption evidence behind that as well. NetSuite, citing Institute of Financial and Operations Leadership research, reported that AI adoption in accounts payable rose from 7% to 29% in one year. That kind of jump usually means teams are seeing something useful enough to keep. (netsuite.com)

The reason AP moves sooner than some other categories is simple. Invoices are structured enough to interpret. Payment workflows are rule-based enough to support. And mistakes are visible enough to catch. That combination gives AI a fair chance to succeed.

Month-end close acceleration

The month-end close is another area where AI is becoming genuinely useful.

Close is one of the most labor-intensive recurring processes in finance. It is deadline-driven, repetitive, and full of work that consumes time without necessarily adding much judgment. That makes it a strong candidate for AI assistance, as long as the team is using it to support the process rather than pretending the process no longer needs human review.

The most practical uses here are reconciliation support, anomaly detection, journal entry preparation, variance flagging, and documentation drafting. None of that eliminates the need for accounting oversight. What it does is reduce the amount of time spent assembling and formatting so the team can focus more of its attention on review, approval, and investigation.

That shift matters. It is one of the clearest examples of how AI is changing the CFO role and the broader finance function. People spend less time buried in mechanical reporting work and more time using judgment where it counts.

Cash flow forecasting

Cash flow forecasting is another category where AI can produce real gains, especially in environments where timing matters and liquidity pressure is real.

Traditional forecasting often depends on assumptions that get updated periodically and manually. AI-assisted forecasting can absorb new information faster, recognize patterns in historical cycles, and surface anomalies earlier as inputs change. That does not make forecasting perfect, but it does make it less stale.

For finance teams, that is a meaningful improvement. Better timing often matters more than theoretical precision. If a system helps the team see a likely problem earlier, that alone can create value.

L.E.K.’s 2025 CFO survey also identified cash flow forecasting as one of the more promising AI use cases in the office of the CFO, largely because it benefits from continuous inputs and faster scenario work. (lek.com)

GAAP compliance scanning

This is one of the more practical use cases that gets less attention than it should.

AI is increasingly useful for scanning financial records for treatment anomalies, classification inconsistencies, disclosure gaps, and other issues that deserve a closer look before they become audit problems. That does not mean AI replaces accounting judgment. It means it can reduce the search burden.

For accounting teams, that is a real advantage. Instead of manually hunting across large datasets for everything that might be wrong, the team can start with what the system already identified as unusual. In practice, that can save time, reduce audit friction, and help surface issues earlier in the reporting cycle.

Financial narrative generation

Narrative generation is not the flashiest category, but it is one of the more quietly useful ones.

Accounting and finance teams spend a surprising amount of time producing recurring written explanation: management commentary, variance summaries, report notes, board package language, and performance narratives. Much of that writing is not difficult, but it is repetitive and time-consuming.

AI is already useful for producing first drafts in this area.

That does not mean the system should be trusted blindly. A human still needs to review the narrative, confirm the framing, and make sure the writing reflects what leadership actually wants to say. But removing the first-draft burden can still save meaningful time, especially during busy reporting periods.

Where the market is still ahead of reality

This is the part vendors usually do not emphasize.

There are still several categories where the sales story is more mature than the production reality. The technology may eventually get there, but that is different from saying it is already dependable enough to build a strategy around today.

Fully autonomous tax filing

AI can absolutely support tax workflows. It can organize information, flag discrepancies, summarize changes, and help preparers move faster.

What it cannot yet do reliably is replace the human preparer in a fully autonomous way across real tax environments. Tax work is full of edge cases, jurisdiction-specific requirements, interpretation issues, and liability-sensitive decisions. Those are not small details. They are the work.

So the right use of AI in tax today is support, not autonomy.

End-to-end FP&A automation

FP&A gets mixed into the same conversation all the time, but it is worth being careful here.

AI can make FP&A better. It can help process larger amounts of data, accelerate scenario modeling, highlight anomalies, and support recurring analysis. What it does not do well enough yet is replace the strategic judgment that makes FP&A valuable in the first place.

Strong FP&A depends on business context, management priorities, market understanding, and leadership interpretation. Those are human functions. AI can support them, but it does not remove the need for them.

Autonomous audit

AI in audit is legitimate. Fully autonomous audit is not.

There is a big difference between using AI to help review documents, identify outliers, and accelerate certain steps in the audit process, and claiming the audit can run end to end without meaningful human oversight. The professional judgment, review obligations, and regulatory stakes involved are still too high for that to be a mature operating reality.

AI can assist audit work. It does not replace the responsibility attached to it.

What separates useful AI from disappointing AI in accounting

Even the stronger use cases do not work equally well in every accounting environment.

Whether AI creates value for your team depends less on the quality of the demo and more on the conditions underneath the workflow.

The first issue is data quality and accessibility. AI does not fix weak accounting data. It exposes the weakness faster. If source documents are inconsistent, fields are incomplete, invoice formats vary wildly, or the needed information is buried across disconnected systems, the tool will run into those problems quickly. That is one reason an AI readiness assessment is worth doing before making a serious buying decision. In most cases, the biggest project risks are already sitting in the data, process, and ownership model before the software ever gets deployed.

The second issue is integration. Most accounting AI tools are only as good as their connection to the ERP, GL, AP workflow, bank feeds, and other systems they depend on. If the integration layer is unreliable, the output quality falls apart fast. This is why a clean demo should never be confused with a proven fit.

The third issue is ownership. AI in accounting still needs a human owner. Someone has to review outputs, manage exceptions, maintain accountability, and decide what gets trusted, what gets escalated, and what remains manual. Teams that treat AI as a supervised workflow tool tend to get better results than teams that assume the software will take care of itself once it is live.

A better way to evaluate AI for accounting teams

At this point, asking whether a platform has AI is not a useful question. Almost every finance platform will say yes.

The better questions are more grounded.

Which workflow is this supposed to improve? Are the inputs structured enough for it to work reliably? Are the outputs easy to verify? How visible are the failure modes? What review process stays in place? What does the integration actually look like in our environment?

Those are accounting questions. They are also the questions that usually separate tools that work in practice from tools that mostly sell a compelling story.

Final thought

AI for accounting teams is real, but it is not evenly real.

The strongest use cases today are not the most futuristic ones. They are the ones where the workflow is structured, the outputs are testable, and the review process already exists. That is why AP automation, close acceleration, cash forecasting, compliance scanning, and narrative generation are moving faster than more ambitious categories like autonomous tax or autonomous audit.

The accounting teams getting the most value are not chasing the broadest claims. They are starting with the workflows that hold up in production, learning what works in their own environment, and building from there.